Rambling through the 2018-19 Financial Results

The Swiss Ramble does a great job of presenting these results in graphics that are easy to understand and then providing useful commentary that summarizes the information. We in turn take these figures and graphics and comment on the results based on what catches our eye.

Overall Results

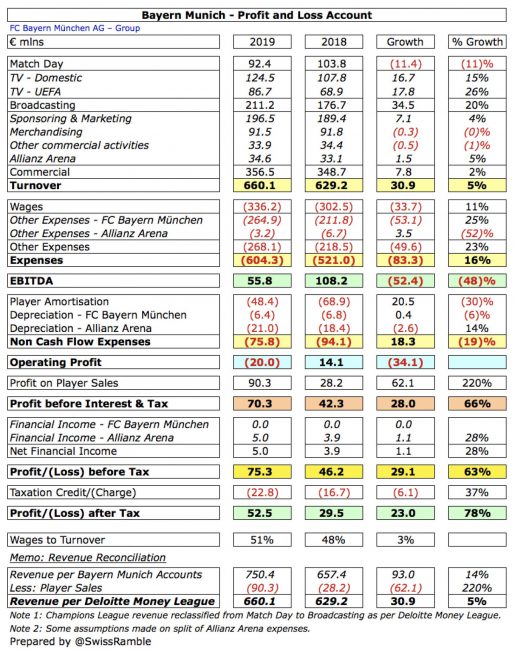

A cursory glance through the 2019 Profit & Loss (P&L) shows another strong year of growth from FC Bayern with a few exceptions. Turnover (revenue) increased €30.9m year over year to €660.1m. Profit before and after tax increased €29.1m and €23.0m year over year to €75.3m and €52.5m, respectively.

On the flip side, Match Day revenues decreased by €11.4m from 2018 to €92.4m, due mostly to staging less Champions League matches according to Swiss Ramble. Expenses notably increased by €83.3m to €604.3m. Earnings before interest, taxes, depreciation and amortization (EBITDA) decreased during the year by 48% to €55.8m. Finally, operating profit declined by €34.1m to €(20.0)m.

The primary factors for these declines were a €33.7m increase in Wages and a €53.1m increase in Other Expenses. The increase in wages is understandable and likely to continue it’s assent but it’s unclear what the driving forces were behind the increase in Other Expenses and is therefore something to keep an eye on going forward.

Impact of Player Sales

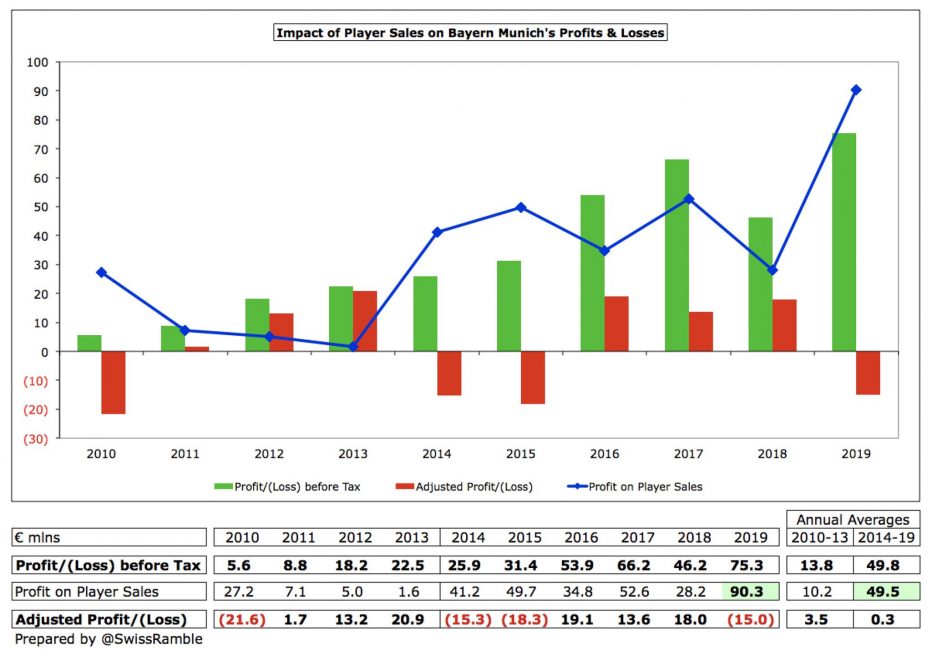

The accounting for Player Sales is always an area of contention between club and auditor. The club includes the profits from player sales in their revenue figures, where the auditors consider these to be extraordinary income.

This had an increased affect on the figures this year as the €90.3m brought in is the highest in club history. If you include Player Sales, Revenues jump up to €750.4m from €660.1m.

On the other hand, if you were to exclude player sales from the P&L before tax, Bayern would drop to a €(15.0)m loss from the €75.3m profit for the year. That number is somewhat alarming on the surface, though clearly player sales factor into how the club runs it’s business.

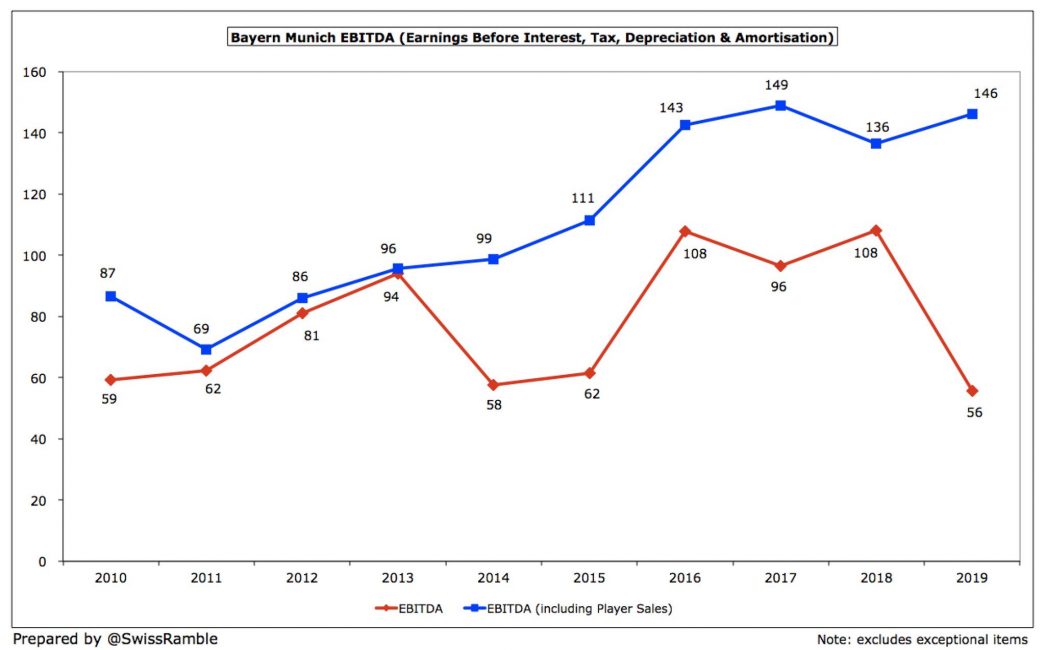

EBITDA is also greatly affected by Player Sales. When including those profits, Bayern are near their historic highs, whereas excluding them puts them at a 10 year low for 2019.

As player sales become more and more regular, it is reasonable to at least acknowledge this revenue source and it’s impact. No matter which side of the argument you fall on, both sets of data provide interesting insight into the club’s performance.

Revenue Up

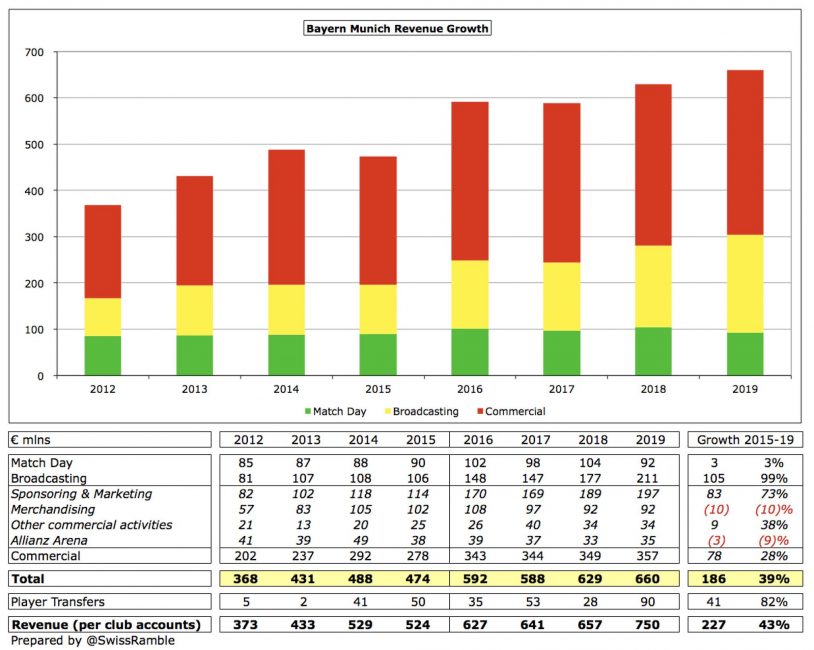

Revenue’s continued their year over year increase in 2019. The graph below breaks down the sources of revenue over the last 8 years which gives insight into where that increase is sourced.

As you might expect, broadcasting revenues are one the biggest factors behind these increases. At €211m in 2019, broadcasting revenues increased €34m over the prior year and €105m since 2015.

Sponsoring & Marketing provides the other significant source of increase having steadily risen for the periods shown. The €197m generated in 2019 is an increase of €8m from 2018 and €83m since 2015.

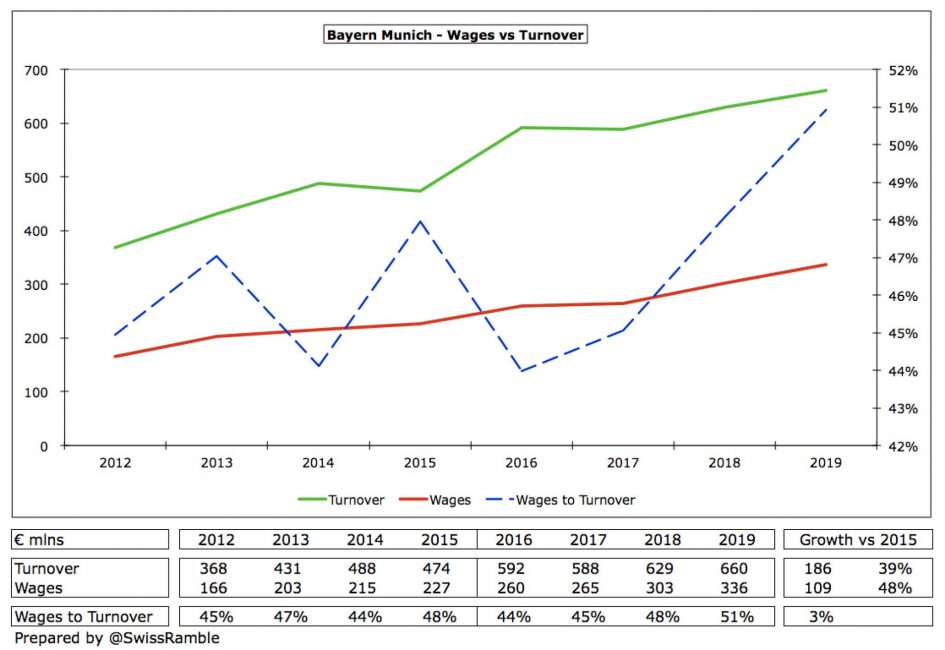

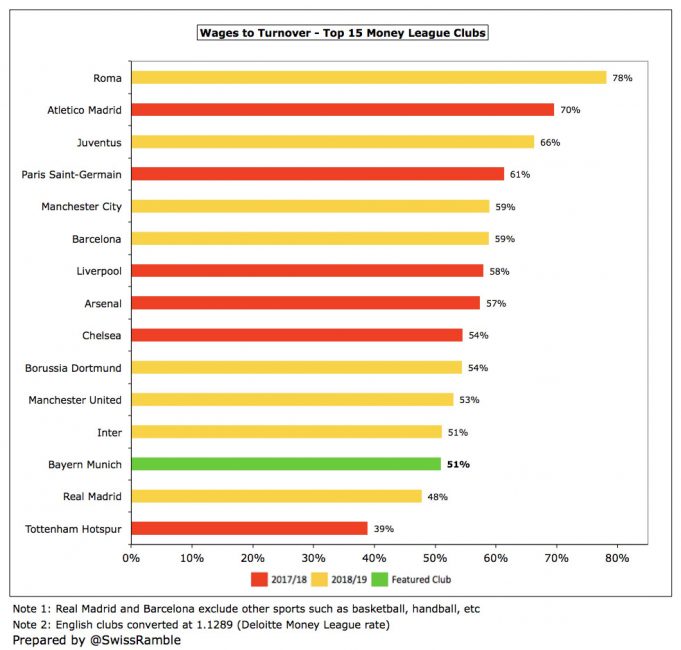

Finally, the offset of Wages and Revenue is an important metric and in 2019 Bayern has for the first time crept above the 50% mark. For the year 51% of their revenue was paid out to their employees. Given the way markets have moved in the last few years, this is hardly surprising, but likely something the Board is keeping a close eye on.

Domestic Dominance

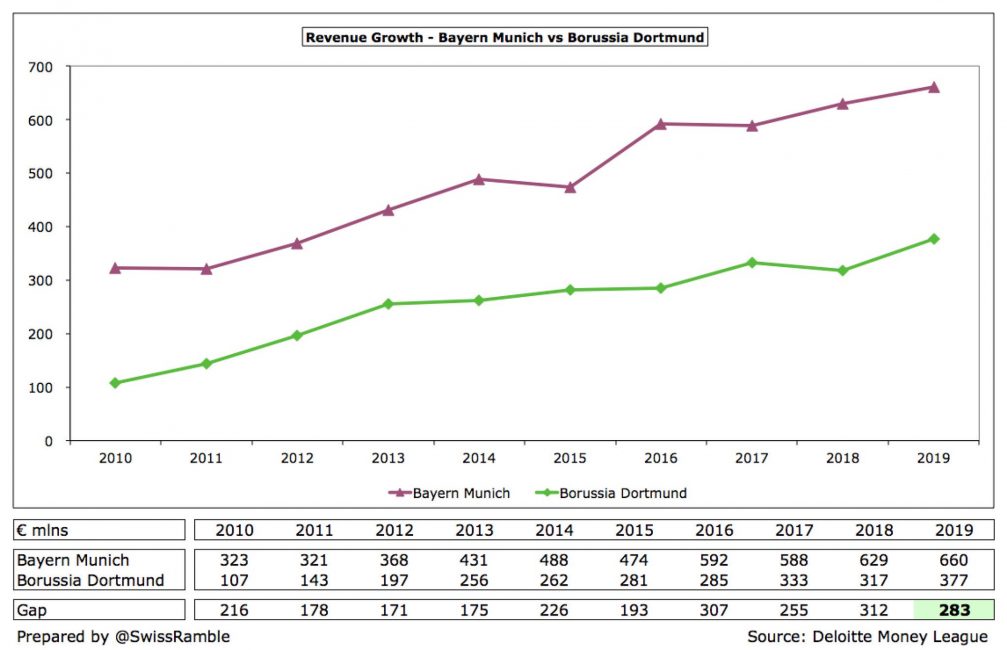

Bayern’s financial performance compared to their Bundesliga rivals is equally as dominating as it has been on the pitch for the last 7 seasons. Once again, the club outperformed their domestic competition by significant margins.

Borussia Dortmund remain their closest competitor but were significantly out performed. While the gap in revenues actually contracted to €283m in 2019 from €312m in 2018, it still represents the 3rd highest gap in the last 10 seasons.

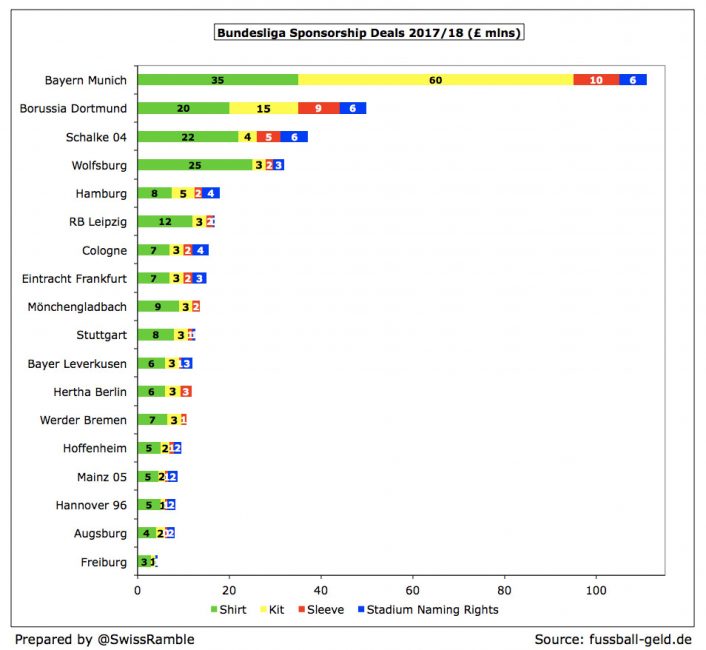

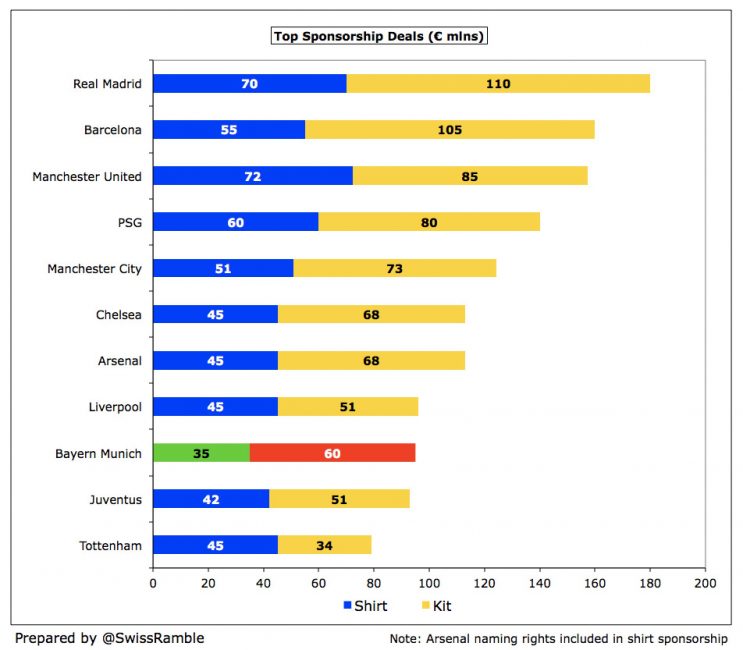

Two of the biggest factors in this split are the differences in sponsorship deals and broadcasting revenues. As you can see in the graph below, Bayern dominate the domestic sponsorship market, with the Adidas deal alone outperforming their next closest rivals entire sponsorship revenue by €10m.

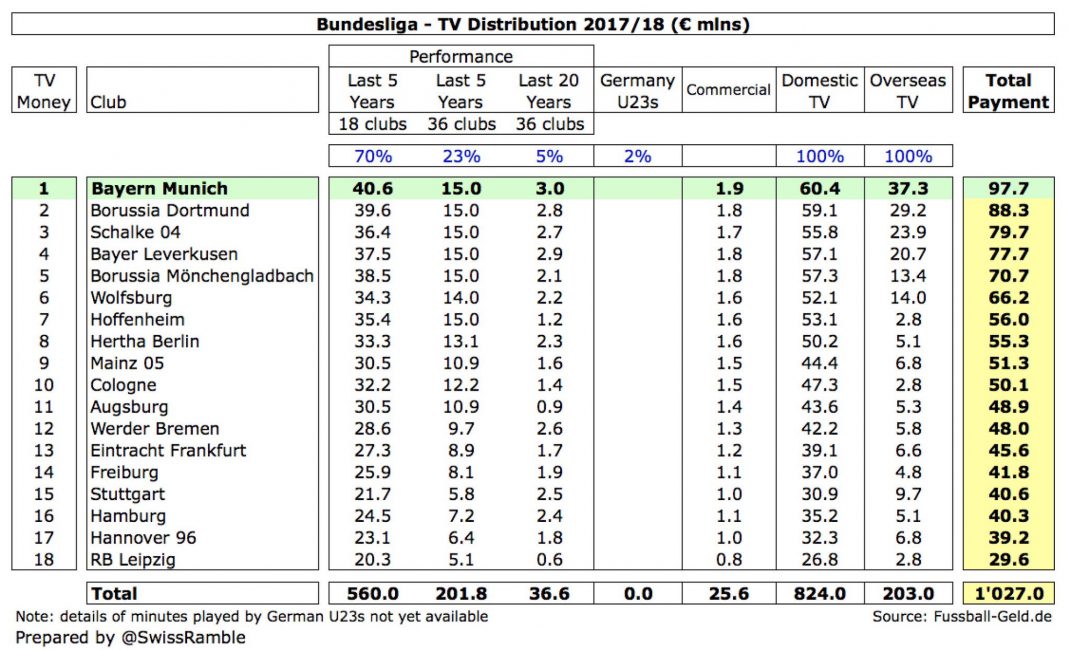

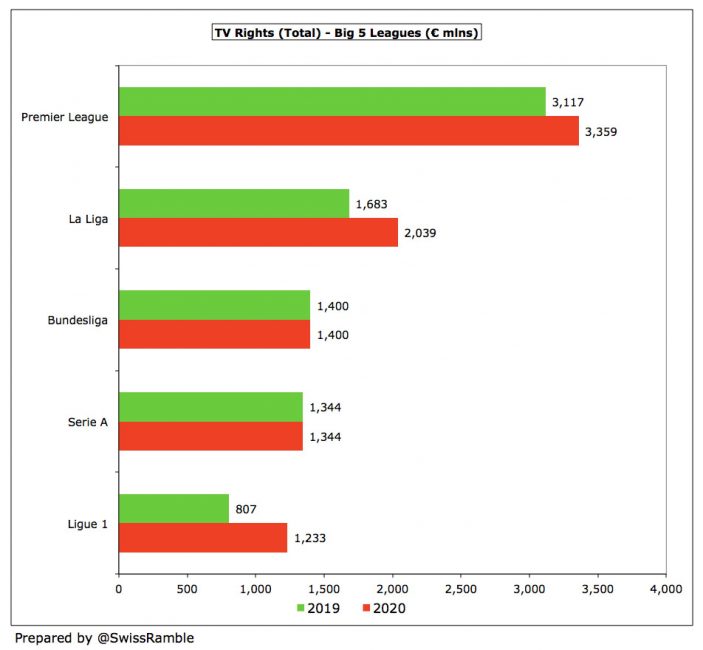

The graphic below gives a breakdown of the Bundesliga broadcasting revenue distribution for the 2017/18 season. Bayern’s unsurprisingly gained the largest payout, a position that is unlikely to change.

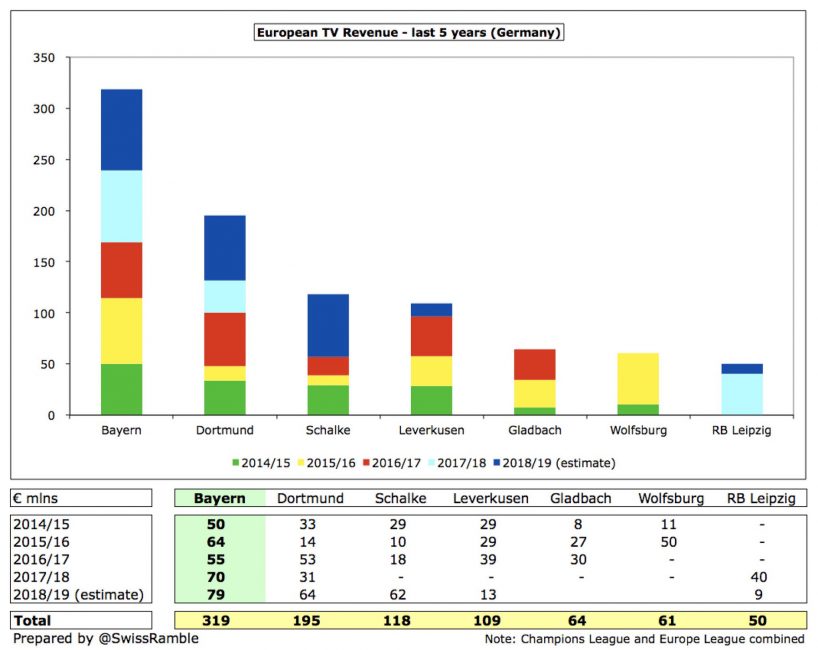

Where the gap really widens though is the European television revenues. Over the last 5 years, Bayern have taken in an estimated €124m more than BVB, their nearest competitors.

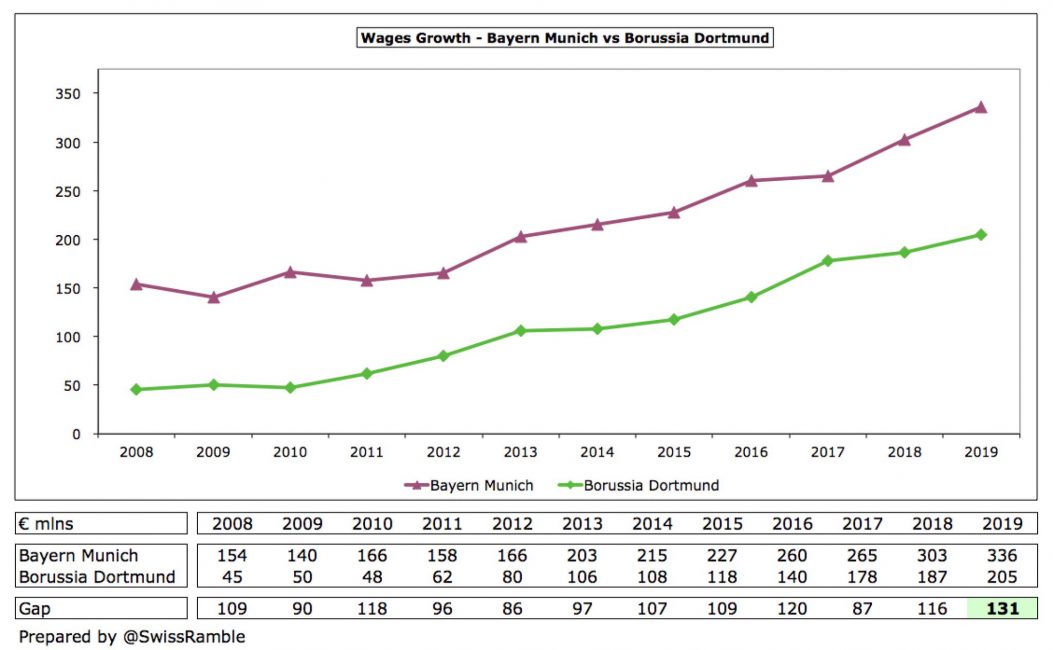

Finally, this difference in revenue between Munich and the rest of the Bundesliga has a major impact on the field as well. In the chart below, you can see that the gap between Bayern and BVB’s wages has reached a 10 year high at €131m.

Interestingly though, Bayern haven’t led the pack in either gross or net spending over the last 4 seasons. RB Leipzig takes the crown as the largest net spenders while Dortmund have spent the most overall, by a significant margin.

Bayern’s advantage over their domestic competition continues to rise. Unquestionably, football lives by the old adage that the rich get richer. While many lament the competitive implications of these numbers, the club deserves credit for their continued financial, and sporting, dominance.

Europe and the Money League

In general, especially given their disadvantage in regards to broadcasting revenue, Bayern performed very well when compared to their European counterparts.

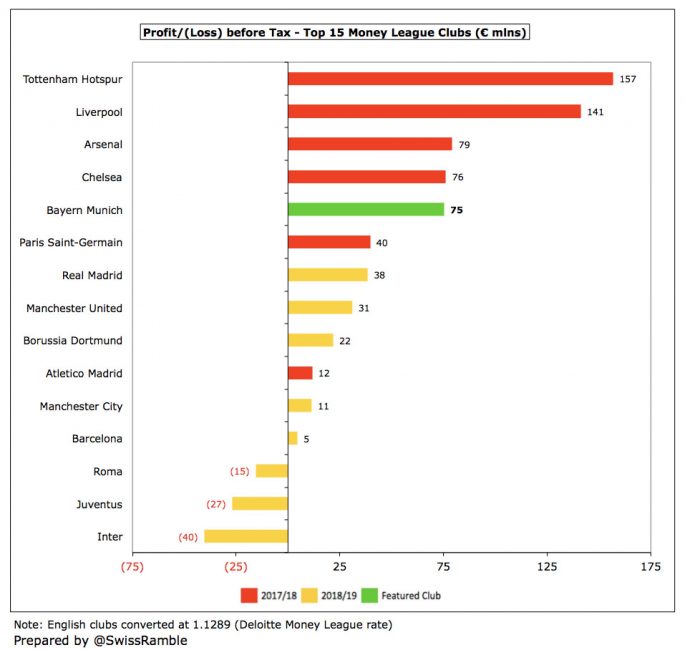

P&L before tax ranks 5th among the top 15 Money League clubs behind four English sides that benefit greatly from their domestic broadcasting deal.

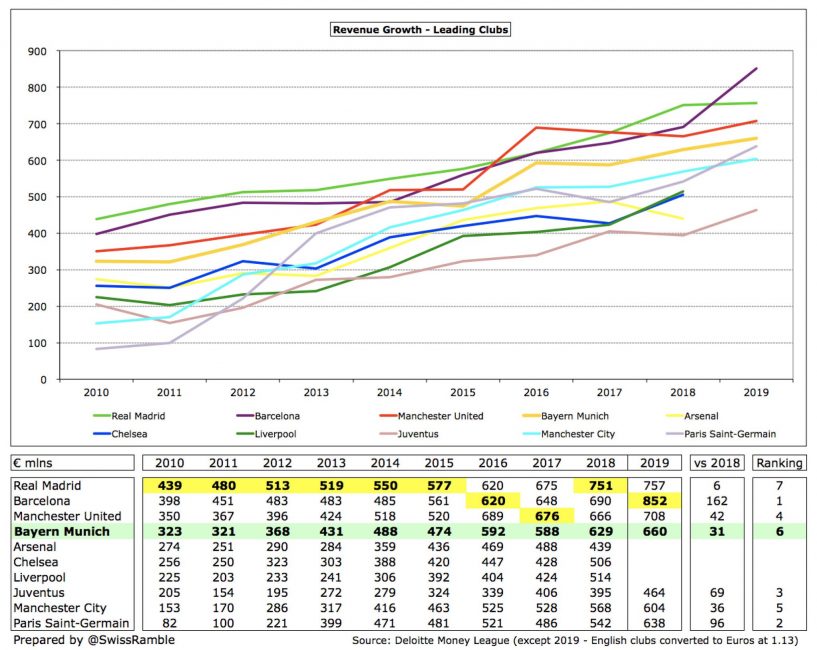

Revenues as well remained strong coming in 4th behind Real Madrid, Barcelona and Manchester United, with Arsenal, Chelsea and Liverpool yet to report.

Revenue growth however was relatively poor to their European competition. Only Real Madrid’s €6m increase was less than Bayern’s €31m. The unfortunate truth is that there is likely very little the Board can do to change this trend, at least in the short term. As the table below shows, broadcasting revenues for the two Spanish giants and the Premier League have launched them into another dimension. Until things change, it will be difficult for Bayern to keep up the pace.

Another area that Bayern are at a disadvantage when compared to their continental rivals is in their sponsorship deals. Bayern may have dominated domestically but are 9th when comparing to their European counterparts.

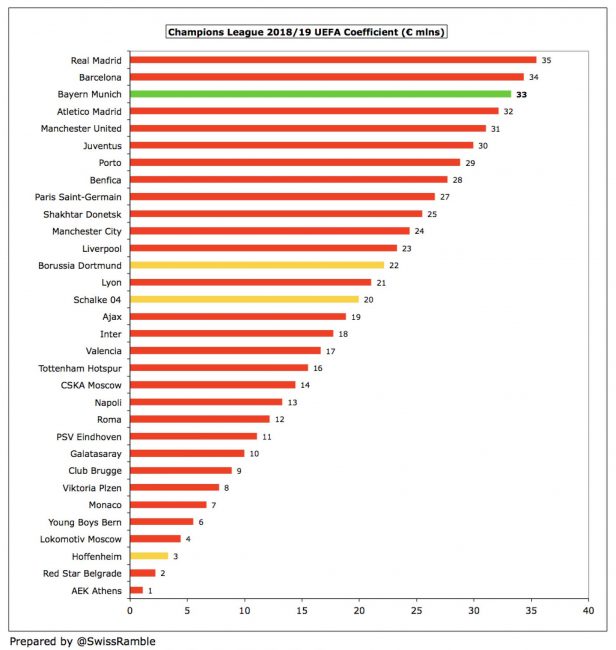

Bayern have given their domestic partners, and in Adidas’s case partial stakeholders, a significant bargain when compared to the other big clubs in Europe. The €35m from Deutsche Telekom for shirt sponsorship is by far the lowest among the 11 clubs examined while the €60m from Adidas comes in at 8th. Both of these seem far too low given the commercial and sporting success that Bayern has enjoyed over their history. As you can see in the table below for example, their Champions League coefficent was 3rd, just behind Real Madrid and Barcelona, which suggests that based on performances they should be much higher in the sponsorship rankings.

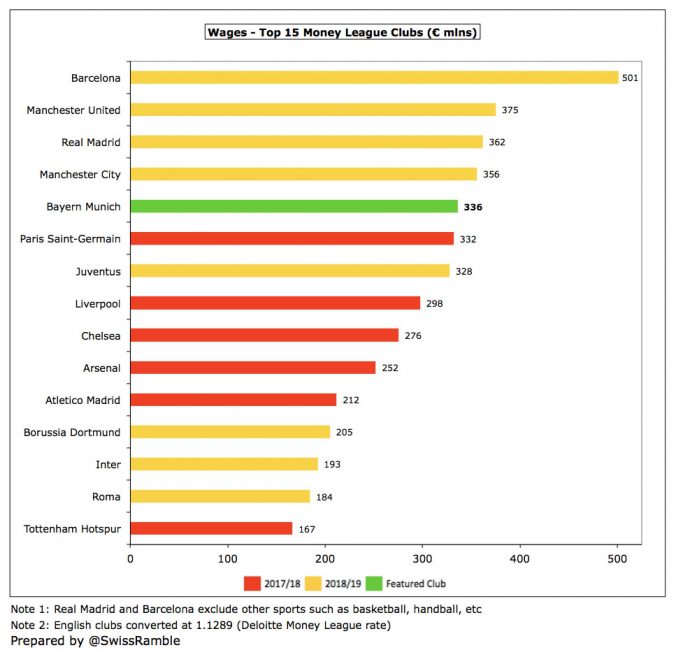

While Bayern is playing at a disadvantage in terms of sponsorship and broadcasting, they have maintained a close distance in large part due to commercial revenues. This has allowed them to keep their wages competitive, which obviously affects their on field success. As you can see below, Bayern had the 5th highest Wages of the Money League clubs.

Importantly though, they managed to pay those wages at a much lower percentage of their total revenues with the exception of Real Madrid (and Tottenham whose wages were also significantly lower). So while that 3% increase to 51% is likely a thorn in the side for the board, it is well below most of their European competitors.

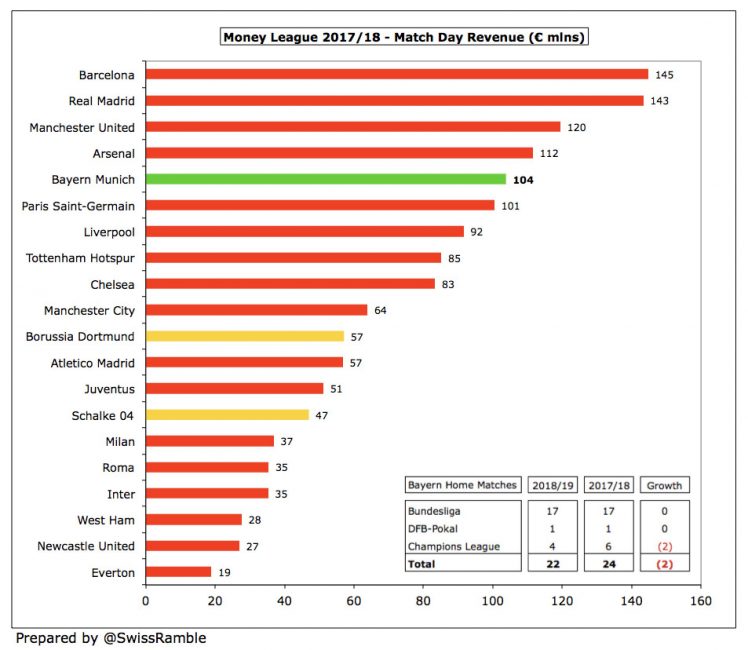

2017/18 Money League

Due to the timing of each club’s filing and the time required to compile data, some metrics are necessarily only comparable for prior periods. The following are largely from Deloitte’s Money League comparison for 2017/18.

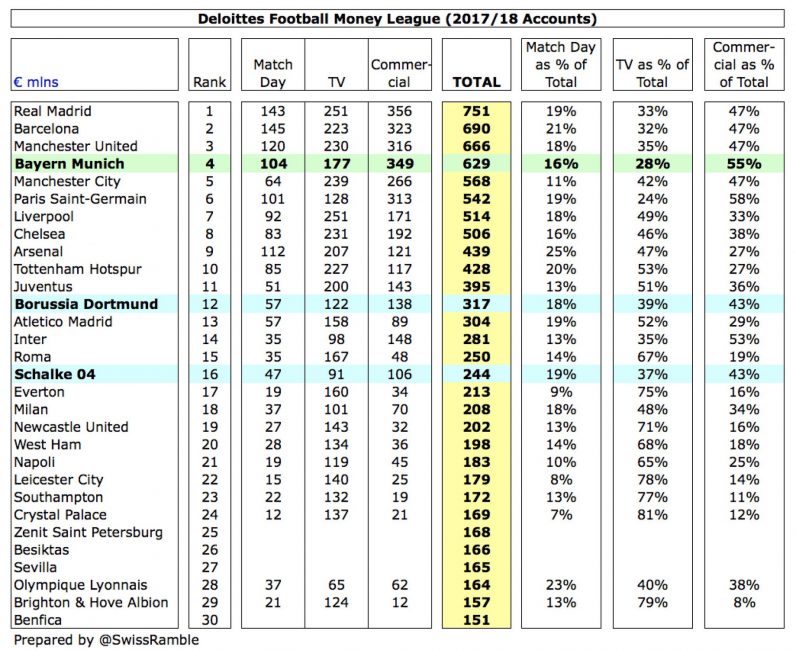

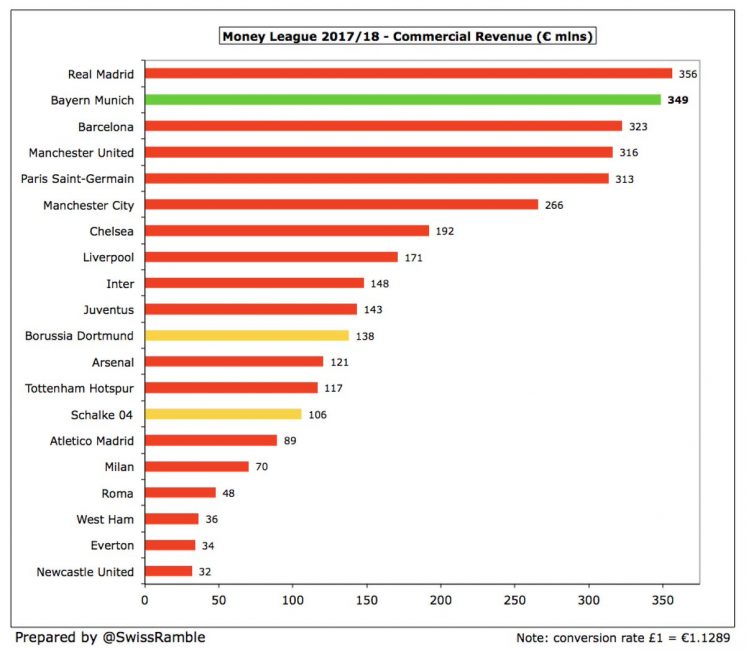

Overall, Bayern finished 4th in the Money League behind Real, Barca and Manchester United. As Swiss Ramble notes, this ranking in terms of revenue could take an adverse hit due to several clubs, including Barcelona and PSG likely surpassing the Munich club in Commercial Revenue.

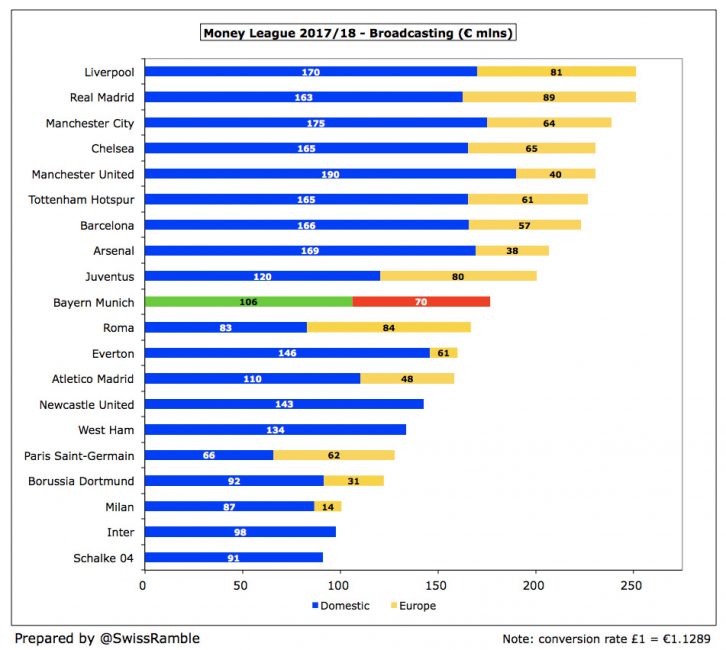

While Bayern finished 2nd last season, many of the clubs in Europe are catching up with or surpassing them in a category that they used to dominate. As mentioned repeatedly, broadcasting revenues are a huge problem for Bayern. Below is a breakdown of how they actually fared.

This graphic puts into stark focus the challenge presented to FC Bayern in regards to domestic broadcasting revenue. Manchester United for instance brought in more from their domestic broadcasting deal than Bayern did in total. Even Premier League clubs with very little to no European revenue are neck and neck with Bayern. Of Europe’s elite, only PSG suffer a worse fate domestically bringing in just €66m.

Finally, Bayern has remained very strong in terms of match day revenues coming in 5th. This is particularly impressive given their ticket pricing structure, which tends to be far lower than the rest of Europe.

Challenging Future

In summary, Bayern had another solid financial year in 2019. While they continued to dominate their domestic competition, the European landscape is murkier. The board will need to be creative to find a way to stay competitive given their domestic limitations.

It will be especially interesting to see how these challenges are faced given the recent shakeups at the higher level. With Uli Hoeneß retiring, Herbert Hainer will need to put his business acumen to good use. He and Karl-Heinz Rummenigge will lead this charge over the next few seasons, as well as Oliver Kahn, who will take over for Kalle in a few years.

Perhaps this is a good thing though. Perhaps new blood will institute fresh ideas that will allow Bayern to maintain their identity while also remaining competitive in Europe. There’s little doubt however that there are many challenges awaiting the Board in the near future. Whether they have the solutions to these issues, remains to be seen.

@Marc

First again congrats on a good analysis of our financials.

I do not know where Swiss ramble got the detailed figures from as they were not published yet in detail.

But assuming they are correct than those financials are confirmed to be worrying as stated on the German side.

BTW why do you not ask Alex to publish them in detail there also?

With regard to analyzing figures I agree that one must exclude player sales from ordinary business income and exclude them thus from ordinary operating business profit or loss.

Of course they must be added to the overall P+L statement thus determining overall profitability.

But even for FIFA s license approval process figures must differentiate transfer income to determine an operating going concern on a 5 year forward basis.

Also UEFA payments should not be considered as commercial income but as TV related income. Swiss ramble should split the broadcasting figures in domestic and international.

Also all major football accountants KPMG Deloitte and Brand Finance differentiate accordingly .

Having said that and on this basis our figures look bleak.

Turnover

It demonstrates the impact of our dismal loss against LFC in the QF. Unfortunately the higher UEFA payments due to a restructured pool hides the fact that they would have been even higher if we succeeded and made it to the SF at least. My guess is we lost overall 35 mio y/y.

As rightly stated we are caught in the central dfl broadcasting deal which we cannot much influence.

Also match day revenue growth is limited although one should look at the lounge marketing and imo too many tickets are given for “free” to sponsors.

Apropos Sponsoring income.

We had been for years the ultimate master in that segment together with MUFC. Now Real Barca and almost all the top 6 EPL clubs are catching up or jumped ahead.

Our sponsor/equity approach with the AAA which was heralded as second to none in the 00’s seem to work detrimental against us now.

Our own shareholder sponsors AAA pay more to other clubs than to us esp. Adidas pay 120 mio to Real and 100 Mo to MUFC compared to 60 mio to us.

DT too although no shareholder but on the board as the 4th key Sponsor pay only a fraction of what Rakuten and Emirates are paying Barca and Real.

Hainer KHR and the board must improve Sponsoring income over the next 2 years significantly , imo by at least 150 mio to compensate.

Expenses:

They are really high and we must wait exactly who or what is in it.

Wages

Assuming salaries are accounted as per 30.6./1.7. correctly then RibRob Rafa Hummels Wagner are coming off the payroll in the current period only but Lucas Pavard Coutinho Perišić are added (leaving out the players with smaller salaries).

Also I guess a considerable increase is related to the academy where new staff and players were added.

Other expenses

We must wait for detailed figures but assume those contain the one off payments for Anc and staff. Also probably agent fees and golden hellos for Goretzka etc. so how much of those are one offs which really should have been segregated as transfer income from ordinary commercial activity.

But the increase is significant and must be explained and observed as it is eating up significantly the operating income.

Another aspects are the depreciation figures.

They are at record low for players and should go up with Lucas Pavard etc . Assuming the transfer expense figure is about 150 mio in the period they will be depreciated over 5 years I.e. 30 mio p.a.increase.

Adding hopefully Sane 100 mio this winter the figure may increase to 50 mio p.a.

And with another 100 mio for Havertz or Coutinho even increase further.

Hence it will decrease our EBT but our tax and dividend payments accordingly.

At the we generate profits and liquidity to invest and maintain a first class competitive squad and not to pay dividends to sponsor/shareholders who even pay us below pari passus vs our competitors.

Probable and possible sales of Boa Javi Tolisso will compensate.

As the contracts for Neuer Müller Alaba Thiago Kimmich Goretzka Gnabry must and will be renewed it is fair to assume that the payroll will stay above 300 Mio and grow further. Hopefully in line with organic growth.

In future player sales and transfer income will become more and more an important factor in our club. The academy will produce many players and most wont make it to our first team and thus will be sold. Thus inadvertently another revenue stream will be established.

We also must note that clubs like MCFC LFC Real Barca CFC Spurs purchased many players well below current market as they were buying constantly in a rising market and /or having managers which increased the players/squad values significantly like Pep Klopp Poch Zidane.

Outlook

We have invested already significantly and will even do more so. It is fair to assume that from 21/22 onwards there will be considerably less squad investment and a period of amortization.

Our liquidity of 200 mio plus shall decrease significantly for a short period but increase quickly again as we won’t have to allocate much for infrastructure maintenance interest.

We must be willing though to invest on a constant basis in our squad and avoid failures for not signing players like Sane KdB Neymar when the opportunity arises.

An intelligent scouting and player assessment department is required to succeed.

Thank you for your praise and carefully crafted response. Swiss Ramble seems to get access to these results somehow each year and I have yet to see any real errors, so I generally trust the numbers that they provide. Your assessments are all logical and well founded and you’ve hit on a few areas that I was unable to really focus on in the article.

For instance, the idea of the new youth academy being an additional revenue stream is an excellent addition and hard to relate with out more detailed figures. I actually would tend to think it is intentional though as the youth academy presents two excellent opportunities for the club that were surely key selling points in the investment in the new facility and players. Obviously, it potentially offers them access to world class players without breaking the bank but as you rightly say, selling those players that aren’t quite up to Bayern’s standard will also provide an influx of cash to reinvest.

In regards to the sponsorship deals, that to me is one of the more concerning areas, especially given how dominant they used to be. I too think it’s ridiculous that Real and ManU’s Adidas deals are so much higher than Bayern’s. If they were at all close I wouldn’t necessarily have a problem with it but there is no reason that the deal should be at half the size of those two clubs. Unfortunately, that contract runs till 2030, so I have no idea how the club can rectify this in the near term. DT’s contract on the other hand ends in 2023. I would expect that Hainer and Kahn/KHR to improve this deal to at least the tier below PSG, in other words somewhere in the 45-50M range, though I believe they should aim higher.

As you noticed, I avoided talking about the other expenses too much, because it’s just too unclear to me if they are one off’s during the year. If that’s the case, it’s understandable and these things happen. If however they are increased recurring expenses, that is something they will need to try to make up for elsewhere.

The depreciation figures was another area that were hard for me to analyze. There just is not enough data to really tell me why that number decreased the way it did though I would hazard a guess it is related to some of the players that came off the books last season and the fact that most of them weren’t replaced in that fiscal year. I would expect that number to be much higher next year, especially if they were to add Sane and/or Havertz.

As you rightly say, it is reasonable to assume that both player salaries and revenue will grow at a similar pace and that those increased profits should go into building/maintaining a world class club. KHR said as much when discussing the results.

Matchday revenue isn’t super concerning to me since the primary factor on fluctuations is the amount of CL matches played. I agree with you that a breakout of CL accounts would be beneficial given the nature of competition. Those numbers can change so dramatically from season to season that it would give a better understanding of the performance related to their ordinary accounts.

Your outlook seems on point. I think your final line will be the crucial factor as to how effective the youth pipeline will generate both cash and first team players.

FYI, I believe Alex will be working on a translation in the next day or two, but no promises.